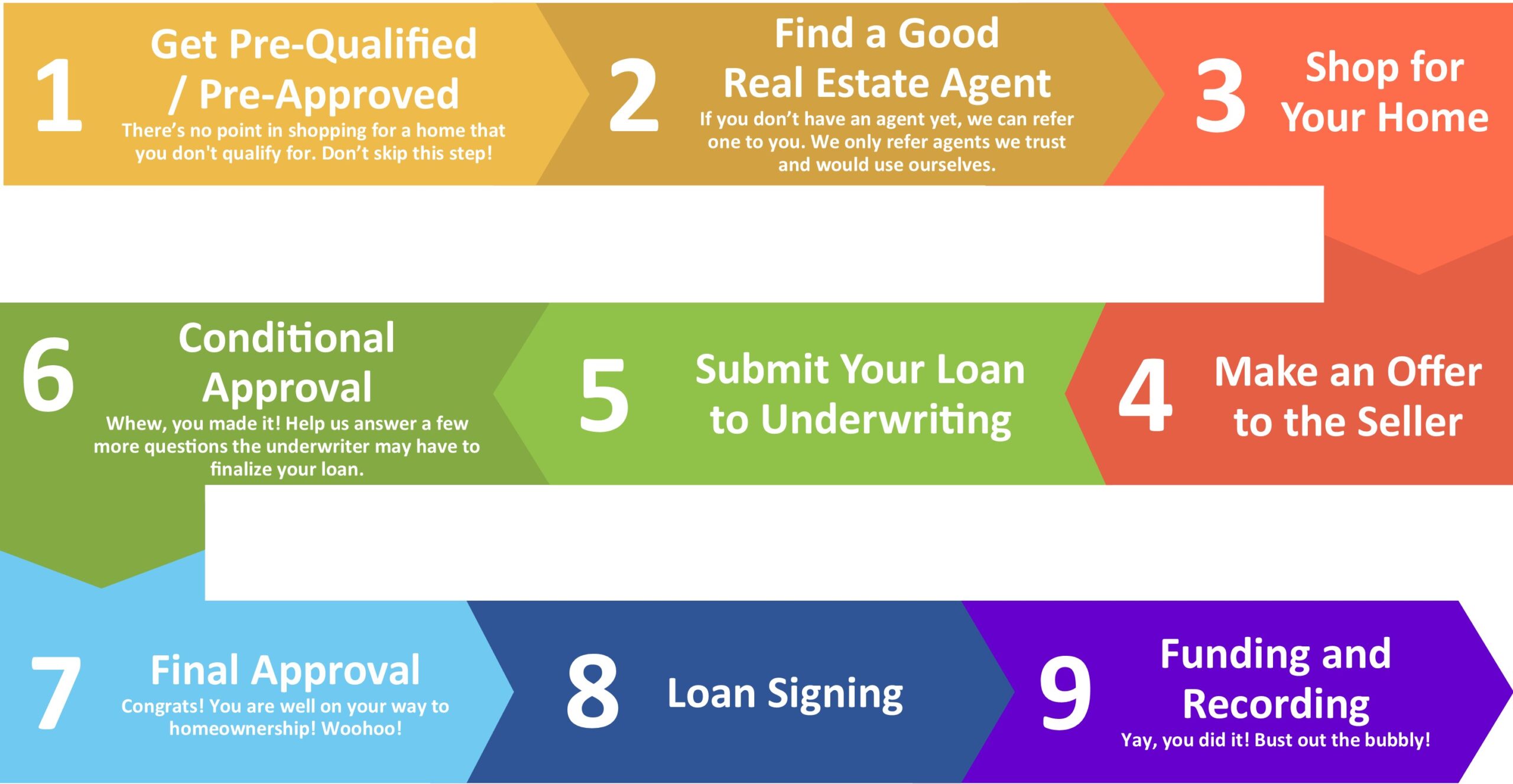

The first step in obtaining a loan is to determine how much money you can borrow. In the case of buying a home, you should determine how much home you can afford even before you begin looking. By answering a few simple questions, we will calculate your buying power, based on standard lender guidelines.

Click here to Pre-Qualify

You may also elect to get pre-approved for a loan which requires verification of your income, credit, assets and liabilities. It is recommended that you get pre-approved before you start looking for your new house so you can:

- Look for properties within your range.

- Be in a better position when negotiating with the seller (seller knows your loan is already approved).

- Close your loan quicker.

More on Pre-Qualification

LTV and Debt-to-Income Ratios

FICO™ Credit Score

Self Employed Borrower

Source of down payment

LTV and Debt-to-Income Ratios

LTV or Loan-To-Value ratio is the maximum amount of exposure that a lender is willing to accept in financing your purchase. Lenders are usually prepared to lend a higher percentage of the value, even up to 100%, to creditworthy borrowers. Another consideration in approving the maximum amount of loan for a particular borrower is the ratio of monthly debt payments (such as auto and personal loans) to income. Therefore, borrowers with high debt-to-income ratio need to pay a higher down payment in order to qualify for a lower LTV ratio.

At Smart Money Hawaii we understand that everyone does not have the same financial goals. We make sure we take the time to discover what your long term goals are in the beginning so that we can tailor each deal to reach your individual goals. We treat each of our clients like we would our friends and family which is why clients come to us for their future purchases or refinances time and time again. Let us prove to you why Smart Money Hawaii has hundreds of 5 star reviews on Google!

FICO™ Credit Score

FICO™ Credit Scores are widely used by almost all types of lenders in their credit decision. It is a quantified measure of creditworthiness of an individual, which is derived from mathematical models developed by Fair Isaac and Company in San Rafael, California. It is based on a number of factors including past payment history, total amount of borrowing, length of credit history, search for new credit, and type of credit established.

Some of our clients may come to us with a credit score too low to qualify for a mortgage. It is situations like this where Smart Money Hawaii’s top-notch service shines thorough. If this has happened to you, we can help by offering suggestions on how to improve your credit scores so you can qualify. We also have extensive knowledge of the different loan types available to those with lower credit scores. Take advantage of our complimentary services today!

Self Employed Borrowers

Self employed individuals often find that there are greater hurdles to borrowing for them than an employed person. For many conventional lenders the problem with lending to the self employed person is documenting an applicant’s income. Applicants with jobs can provide lenders with pay stubs, and lenders can verify the information through their employer. In the absence of such verifiable employment records, lenders rely on income tax returns, which they typically require for 2 years.

If you are self employed, don’t worry! We work with our clients closely to overcome any hurdles that arise and have successfully helped thousands of self employed borrowers finance the home of their dreams.

Source of Down Payment

Lenders expect borrowers to come up with sufficient cash for the down payment and other fees payable by the borrower at the time of funding the loan. Generally, down payment requirements are made with funds the borrowers have saved. Documentation showing the borrower has had the funds for the past 2 months are needed to satisfy anti-money laundering laws. If a borrower does not have the required down payment they may receive “gift funds” from an acceptable donor with a signed letter stating that the gifted funds do not have to be paid back.

Connect with one of our experienced loan officers and apply for a loan today