When it comes to accessing the equity in your home, homeowners in Hawaii have several options. Two of the most common ways to tap into your property’s value are reverse mortgages and cash‑out refinancing. Each has its unique advantages, considerations, and ideal use cases. Understanding the differences can help you make an informed decision that fits your financial goals and lifestyle.

At Smart Money Hawaii, we have helped countless families explore their home financing options, and our goal is to provide clear, practical information so you can choose with confidence.

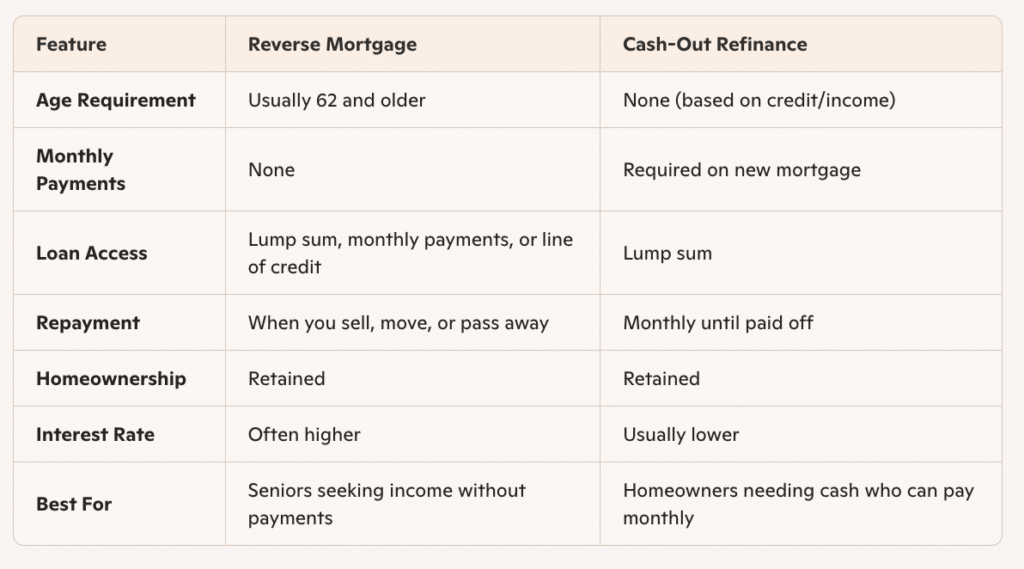

What Is a Reverse Mortgage?

A reverse mortgage is a type of loan available to homeowners typically aged 62 and older. It allows you to convert part of your home equity into cash without having to sell your home or make monthly mortgage payments. Instead, the loan balance grows over time and is repaid when you sell the home, permanently move out, or pass away.

Key Features of a Reverse Mortgage

- No monthly mortgage payments: Unlike a traditional mortgage, you do not make monthly payments to the lender.

- Access to cash: You can receive funds as a lump sum, line of credit, or monthly payments.

- Homeownership remains: You retain title to your home and can continue living there.

- Responsibility for taxes and insurance: Homeowners must continue paying property taxes and homeowners insurance and maintain the home.

- Loan repayment: The loan becomes due when the home is sold or the borrower permanently leaves.

A reverse mortgage is ideal for seniors looking for supplemental income, especially those who want to stay in their homes and maintain their lifestyle without taking on new monthly payments.

What Is a Cash‑Out Refinance?

A cash‑out refinance is another way to tap into your home’s equity. With this option, you replace your existing mortgage with a new, larger mortgage. The difference between the old loan and the new loan is given to you in cash, which can be used for home improvements, debt consolidation, or other major expenses.

Key Features of a Cash‑Out Refinance

- Monthly payments continue. Unlike a reverse mortgage, you continue making monthly mortgage payments on the new loan.

- Access to a lump sum. You receive the cash upfront and can use it as you see fit.

- Interest rates may be lower. Depending on the market, your new mortgage may have a lower interest rate than your original loan.

- Eligibility considerations. Lenders typically require good credit and sufficient home equity, usually up to 80 percent of the home’s value.

A cash-out refinance is generally best for homeowners who are comfortable continuing monthly payments and want a lump sum for specific financial goals.

Comparing Reverse Mortgages and Cash‑Out Refinances

Understanding the differences between these two options can help you determine which aligns best with your financial needs and lifestyle.

Benefits of Each Option

Reverse Mortgage Benefits

- Provides cash without monthly payments: This can be particularly helpful for seniors on a fixed income looking to supplement retirement funds.

- Flexibility in receiving funds:

Whether you need a steady income stream or a line of credit for unexpected expenses, reverse mortgages offer multiple options.

- Home remains your own:

You continue to live in your home, preserving stability and comfort.

Cash‑Out Refinance Benefits

- Potentially lower interest rates:

Your new loan may have a more favorable rate compared to credit cards or other loans. - Lump-sum access:

Perfect for major expenses like renovations or consolidating high-interest debt. - Tax considerations:

Interest on the new loan may be deductible if used for home improvements, subject to IRS rules.

Key Considerations Before Making a Decision

Before choosing a reverse mortgage or cash‑out refinance, it is important to evaluate your circumstances:

- Monthly cash flow needs: If you need monthly income without new payments, a reverse mortgage may be more suitable.

- Ability to handle payments: If you can manage monthly payments and prefer a lump sum, a cash‑out refinance could be a better fit.

- Long-term financial goals: Consider how each option affects home equity, inheritance plans, and overall financial strategy.

- Eligibility requirements: Reverse mortgages have age requirements, while cash‑out refinances require credit checks and sufficient equity.

Choosing the Right Option in Hawaii

At Smart Money Hawaii, we understand the unique financial needs of homeowners across the islands. Hawaii’s high property values and cost of living make it essential to choose wisely when tapping into your home’s equity. Our team can help you:

- Compare reverse mortgage and cash‑out refinance options

- Assess your eligibility and potential loan amounts

- Guide you through the application process with clarity and care

Conclusion

Both reverse mortgages and cash‑out refinances offer homeowners ways to access their home equity, but they serve different purposes. Seniors seeking supplemental income with no monthly payments often benefit from a reverse mortgage. Homeowners looking for a lump sum while maintaining monthly payments may find a cash‑out refinance more suitable.

By carefully evaluating your financial goals, income needs, and long-term plans, you can select the option that best fits your lifestyle. At Smart Money Hawaii (NMLS ID #273384), we are committed to helping you understand your options and guiding you through a transparent, stress-free process.

Take the next step today. Contact Smart Money Hawaii at +1 808-447-1850 or email us at admin@smartmoneyhawaii.com to explore your reverse mortgage or cash‑out refinance options and secure the solution that is right for you.